March 2023: The Debt Doom Loop

Investing in a sovereign debt crisis

“Inflation peaked. But it is not the last peak of this cycle. We are likely to see CPI lower, possibly negative in 2H 2023, and the US in recession by any definition. Fed will cut and government will stimulate. And we will have another inflation spike. It’s not hard.”

– Michael Burry, Scion Asset Management

The sovereign debt crisis the West finds itself in today is the biggest macro-economic theme of our time. The evidence that the debt is out of control is ironclad, the implications for investors and society at large are enormous, yet the topic is extremely underreported. Asset managers and investors are unprepared for a lengthy period of structurally high inflation.

The status quo equity and bond portfolio worked for a long time and few investors active today remember a US dollar pegged to gold, before 1971. It is therefore easy to fall for recency bias – to assume that the inflation and downturn of 2022 was a blip, and that all investors need to do is to “buy the dip”.

Contents

Performance

Inflation comes in waves

Sovereign debt crisis

The debt doom loop

Bretton Woods III

Sound money assets

How to invest in sound money assets

Bitcoin – own the underlying

Portfolio

Final thoughts

Performance

YTD: -5%

2022: +1%

2021: +10%

2020: +49%

2019: +51%

Inflation comes in waves

Inflation often comes in waves. Declining inflation this year does not mean we can count on returning to, and staying at, the CPI levels of the last decade. We could just be over the peak of the first wave. A return to rate cuts and QE when inflation appears solved at the expense of the economy could spur a second wave.

Sovereign debt crisis

“The national debt looks unsustainable, yes, but nothing catastrophic has happened so far.”

This is a common sentiment, the implication that, as the meteorite has been hurtling towards Earth for so long, it may never arrive. Clearly, if one believes we are on collision course with meteorite, that state will come to an end. It’s only a question of when it will hit – is it many decades in the future or will it happen much sooner?

The US national debt is at $31.6tn, or $247,000 per taxpayer. Let that sink in.

In Q4 2022, the interest expense on the debt was $213bn, $30bn more than in the prior quarter, the largest quarterly increase on record.

We’re therefore at around $850bn interest expense annualised on Q4 numbers – it’s more than doubled in a few years. Yet, interest rates are higher now than the average in Q4 and the full impact of the rate rises will only be felt over time as the government bonds in issue mature and have to be replaced at the higher yields.

The US Treasury Department has provided a list of all its outstanding bonds: 30% mature by January 2024 and 52% within three years. These bonds will all have to be refinanced at market rates.

The Treasury’s interest expense already increased from 1.8% to 2.4% between September 2021 and September 2022, and it is set to increase by another 2 percentage points over the next three years. This, including the impact of deficits adding to the debt, equates to the government’s interest expense rising to $1.2tn. This is 25% of current federal spending, which is unprecedented.

It seems, practically speaking, impossible for the government to raise that much by taxation or spending cuts. The only option available is to lower rates, issue more debt and print money to buy back the debt.

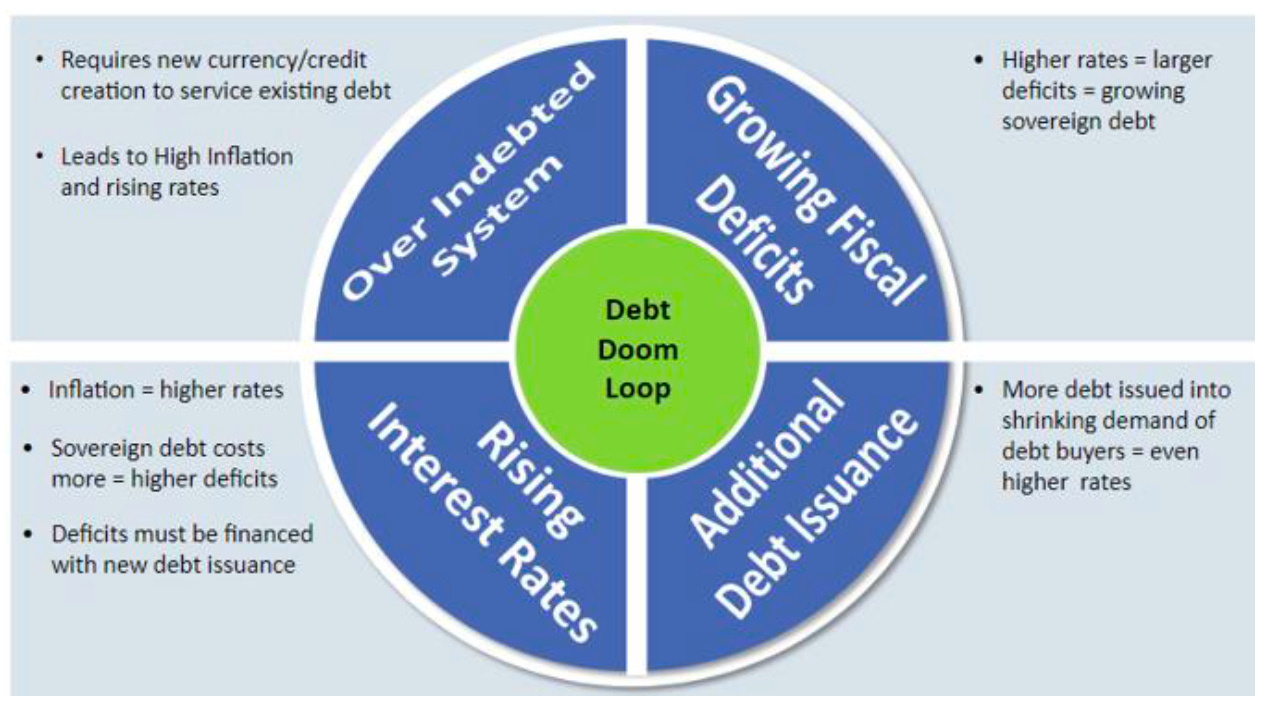

The debt doom loop

It gets worse. Lawrence Lepard, Managing Partner and Portfolio Manager at EMA, in his Fourth Quarter Report, makes the point that the deficit of $1.4tn for the last fiscal year included $600bn capital gains taxes from the bull market of 2021, which will not be repeated for the next period which will include the down year of 2022. Higher interest rates and increased public spending will add to the deficit for this year.

The Treasury estimates $1.3tn in new borrowings for this year, which implies a $2.6tn deficit according to Lepard. In addition, if we enter a recession, tax revenues will fall and expenses are likely to increase for unemployment and social spending, meaning the deficit will increase further and more debt will have to be sold.

The situation is simply unsustainable and the Fed is going to be forced to pivot before long. If the Treasury can’t afford to service the debt at these higher rates, the Fed will have to engage in yield curve control, like Japan, by buying the bonds themselves to keep the yields in check.

Debasement is the only option – we should expect higher inflation over the longer term.

Even a policy of running inflation deliberately hot, however, does not solve anything. Once more people understand this is the situation, they won’t be keen to buy Treasuries at a negative real yield. Once that happens, a ‘dept doom loop’ ensues where the Fed is forced to issue more and more debt to cover higher interest expenses and print dollars in ever increasing amounts to buy it back, accelerating inflation.

Bretton Woods III

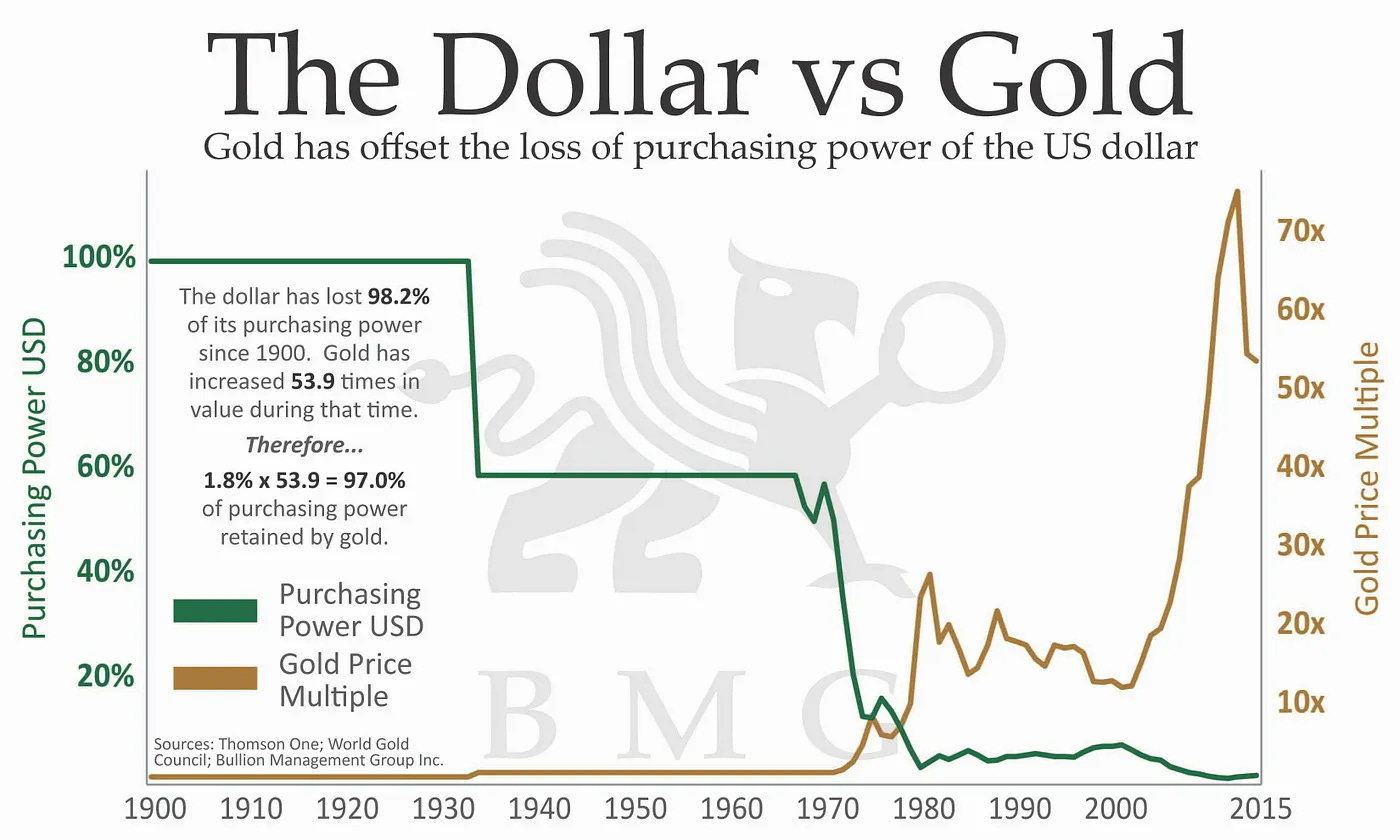

At some point, there has to be a currency reset like we had in the 1970s. A new dollar will have to be pegged to sound money assets. This may come across as a crazy idea – but that is only because the monetary events of the 1970s, and the system that went before where the dollar was pegged to gold, have largely evaporated from our collective consciousness. The modern dollar as a fiat currency only dates back to 1971.

The Bretton Woods monetary system was established in 1944 between the US, Canada, Western European countries, Australia and Japan. It required countries to guarantee convertibility of their currencies to the US dollar, with the dollar convertible to gold bullion. In 1971, the US terminated convertibility of the dollar to gold, an effective default. This brought the Bretton Woods system to an end and ushered in the dollar as we know it – as a fiat currency – and the modern system, sometimes called Bretton Woods II.

Credit Suisse economist Zoltan Pozsar has a thesis that the seizure of Russian assets in 2022, and BRICs countries wishing to settle for oil and gas in currencies other than the dollar, has accelerated the transition to a new monetary system that he calls Bretton Woods III. He imagines this new system will be backed by a basket of neutral reserve assets including gold, oil, natural gas and other commodities.

“…five-year forward five-year inflation breakevens should be discounting a world in which oil and gas is invoiced not only in dollars but also renminbi, and in which some oil and gas is not available for the West at low prices (and in dollars) because they have been encumbered by the East.”

– Zoltan Pozsar, War and Commodity Encumbrance – on President Xi’s speech on settlement for oil and gas in renminbi

Sound money assets

If we do have a prolonged inflationary environment, a decade of successive waves of currency devaluation, investors are under-exposed to the types of assets likely to do best. (Real estate is an exception, but current interest rates are a major headwind for real estate in the shorter term.)

Sound money assets, gold and silver – and, I would argue, new contender bitcoin – are under-owned and under-priced, as are commodity equities.

Commodities are backed by energy, in that it costs energy to extract them, and they can’t be printed. If costs rise over time in fiat currency terms, commodity prices ultimately follow. Oil is the most important commodity in the world as it is used to extract all the others.

Energy and Materials collectively make up less than 10% of the MSCI World Index, less than 8% of the S&P 500, and many investors have even lower exposure than that due to active management and ESG mandates.

How to invest in sound money assets

Macro investing is hard as you have to be right twice: about the macro trend and about the vehicle you pick to play it.

There’s a lot to be said for keeping it simple when it comes to picking the vehicle. You don’t want to be right on the macro but still make no money because of trying to be too clever with security selection.

Buying the underlying commodities is the simplest option but also the lowest return potential. It makes the best sense for bitcoin in my view just to own the underlying asset. I’ve also been considering buying a uranium holding company for uranium exposure. My preference as a value investor, however, is to own cash flowing companies with upside torque to sound money assets.

An ETF of miners or oil and gas producers could be a good choice to purely make a macro bet.

My aim, however, is to find companies that are cheap at current commodity prices, so that the investment should generate a positive return even if commodity prices remain flat or decline slightly, and giving extra upside in the case of rising prices.

In mining, for the expert, selecting small cap miners has the highest return potential. However, this is an extremely tough sector that, in aggregate, destroys capital, so you’re swimming against the tide. It’s also very volatile and small cap mining investors need to put in a lot of work and be very diversified. For the non-expert, this is the type of approach where one would be likely to lose money even if right on the macro. Large and mid-caps, at a good price, are the obvious choice for the generalist investor.

Royalty companies are perhaps the most attractive in an inflationary environment, as royalty companies get the upside of rising commodity prices with none of the increasing capex costs. This is the superior business model – they’re a no-brainer if you can get them at a reasonable price, but they often come with a hefty price tag.

Bitcoin – own the underlying

The upside potential is so great for bitcoin, as it’s starting from a much smaller base than the established hard money, gold, that it’s unnecessary to layer additional risk on top of it. It’s also difficult to find a bitcoin business that gives attractive risk-reward – bitcoin mining profitability is a different game to bitcoin price and this is a very capital intensive industry.

Part of the case for bitcoin is as a bearer money that works outside of the financial system. In a case of a government controlling or limiting fiat transactions, bitcoin will still work as money – which doesn’t apply if you own an equity that needs to be sold for fiat currency.

I do own some MicroStrategy (MSTR) in an UK ISA for bitcoin exposure without tax liability, but most of by exposure is to the underlying bitcoin, self custodied, which is not included in the stock portfolio.

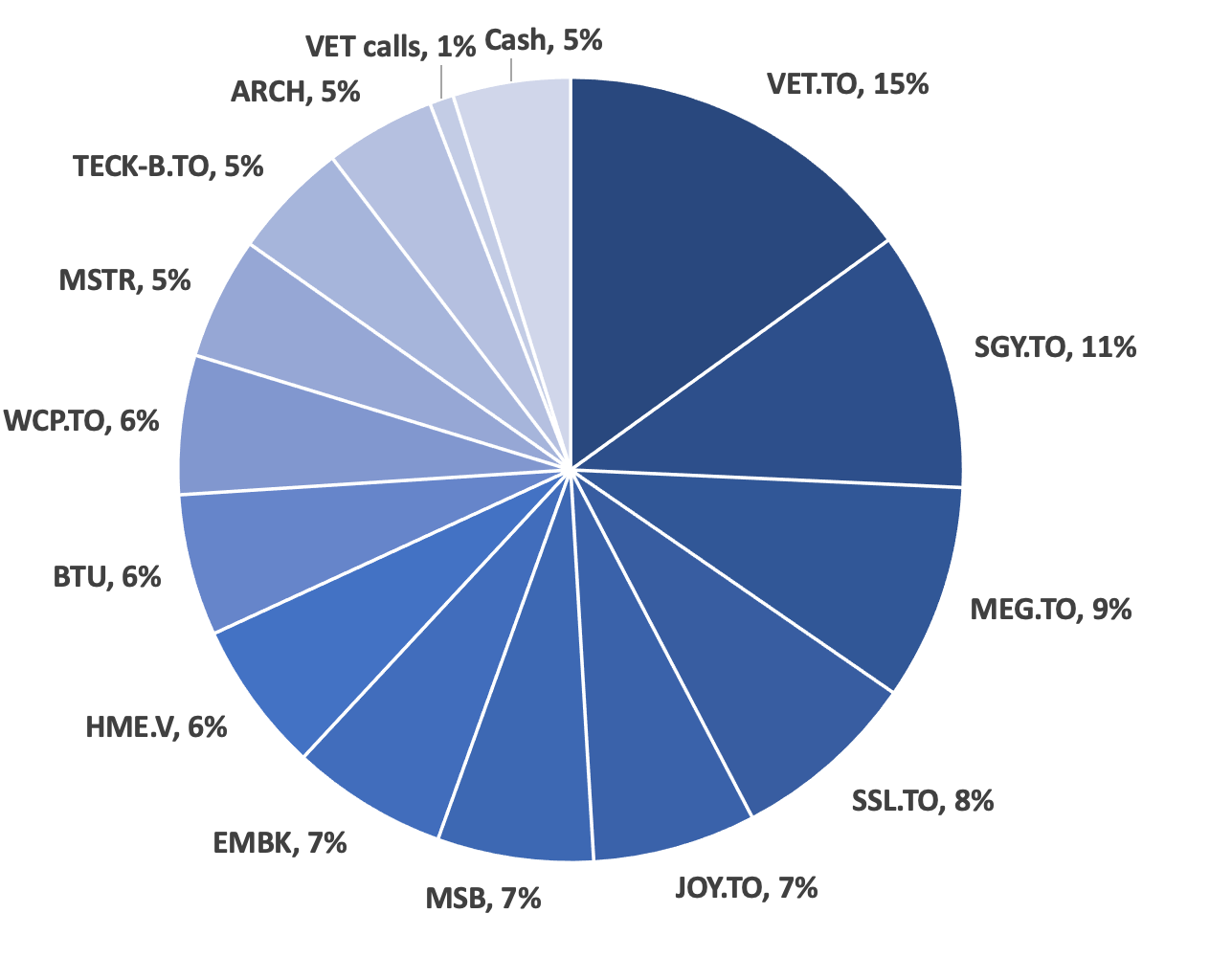

Portfolio

In February, I trimmed some JOY.TO, SGY.TO and ARCH.

I bought some SSL.TO.

I still hold some cash from the sales which I plan to use to buy a new position or add to an existing position.

Final thoughts

Waiting around for the next oil bull run through a bear market can get quite draining. I’m planning to sit tight and not make many alternations to the portfolio. In the meantime, I’m spending a lot of time with the family!

With best wishes,

Timothy Lamb.

Written by Timothy Lamb

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclosure:

The writer owns shares in the securities listed in the stock portfolio at the time of writing.

Disclaimer:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product. Please see the full disclaimer on the About page.