November 2022: Pivoter Is Coming

Why a Fed policy pivot is guaranteed and how this can inform our investment decisions

Dear reader,

This month, I’m laying out my thoughts on why I believe a Federal Reserve (Fed) policy pivot is guaranteed and how this thinking can inform our investment decisions at a high level.

A housekeeping note: those of you who have recently subscribed to the Substack may also like to sign up to the blog mailing list. From this list, I will email occasional blog posts and may also send out a note if I make a change to the portfolio I deem to be of special importance, as I did recently with the sale of the VET calls.

Performance

YTD: +22%

2021: +10%

2020: +49%

2019: +51%

Contents

“If you don’t make stuff, there is no stuff”

The two amigos, Biden & Powell

Pivoter is coming

Prepping for the pivot

Portfolio

Trades in October

Final thoughts

“If you don’t make stuff, there is no stuff” – Elon Musk

During the Covid lockdowns, central banks printed money, people were paid not to go to work and stimulus cheques found their way to the bank accounts of most Americans. We saw the result: there was all this extra cash in the system, combined with broken supply chains and shortages – the perfect recipe for inflation.

Yet, central bankers were somehow caught off-guard. Their education had been the response to the Great Financial Crisis, which had taught them that printing money into a melt-down didn’t cause inflation.

The major differences this time around were 1) that the printed money ended up in people’s bank accounts and 2) we had scarcity.

In supply-driven inflation, it’s the scarce goods and services that act as a match to the bonfire of broader inflation. And we find ourselves, in particular, short of energy, an expense that finds its way into every area of the economy and our lives.

Oil, gas and coal are still the building blocks of our entire global civilisation, and a decade of underinvestment in energy supply, culminating in a global shutdown, would almost certainly have had a broad inflationary effect even without the Covid stimulus. Combined with the stimulus, however, and many other supply constraints, we had the perfect storm for inflation to erupt.

And, at a time of sky-high debt to GDP ratios, we now find ourselves hopelessly lacking the tools to reign it in.

The two amigos

Fed Chair Jerome Powell and US President Joe Biden are the two amigos, going for an all-out, two-pronged attack on oil.

Biden is Chief Supply Officer, emptying his clip – the Strategic Petroleum Reserve (SPR) – onto the market, while campaigning for the world to pump more oil AND simultaneously to sell it cheaper!

Powell, at the Fed, meanwhile, is Chief Demand Officer, raising interest rates at breakneck speed to cause some unemployment and impoverish enough people to kill some demand.

Both of them have found their guns are full of blanks.

The US had large emergency oil reserves, but Biden has squandered this inheritance.

By using the SPR simply to lower gasoline prices for Americans rather than to alleviate an actual supply shortage, he has discouraged investment in supply growth – and, embarrassingly, OPEC+ has now cut production in response. Once the SPR is depleted, he risks leaving the US with both higher prices AND no emergency reserves.

Meanwhile, Powell at the Fed has all of one button to push: to raise interest rates and let the bonds on the Fed’s balance sheet mature. The theory is higher rates will damage the global economy enough to reduce demand (or at least reduce demand growth in the case of oil!).

Like Biden’s SPR policy arguably already has, Powell’s rate rises could also backfire spectacularly. At a time of such high debt, it’s not at all clear that adding to companies’ and individuals’ interest expenses won’t actually worsen inflation. Companies could seek to pass on their higher interest costs to consumers. Workers could then demand greater pay rises to cover these costs and their higher mortgage expenses. Governments could issue ‘inflation relief payments’, as in California. Stagflation spirals.

For energy companies, a recession combined with high borrowing expenses could further starve investment and deepen the oil supply deficit further down the line.

Pivoter is coming

A terminal federal funds rate of over 4%, as is being targeted – or even of 3% – can’t be sustained. As we established in the October newsletter, with just a ~3.2% interest rate on all the US national debt, the interest expense would be $1 trillion a year, which would bankrupt the US.

Harris Kupperman (Kuppy), CIO of Praetorian Capital, says it most concisely with his series of articles titled, ‘The Fed Is Fuct’!

It goes something like this:

The US Treasury is already unable to cover its interest expense without borrowing more to do so.

In the case of continued tightening, the Treasury’s interest expense would rise.

At the same time, recession would result in reduced tax receipts.

The Treasury then has to issue even more debt to meet its expenses.

The Fed is also supposed to be selling bonds (QT).

There are not enough buyers to absorb the new debt.

Yields rise further, which perpetuates the cycle until a bond market collapse.

To avert this scenario, the Fed would have to pivot, buy up the bonds and cut interest rates.

Powell is backed into a corner. As current interest rates can’t be sustained, there is no alternative to a Fed pivot. With the Fed knowing this, I’d imagine they’ll do it sooner rather than waiting until the Treasury market collapses.

The pivot could be prompted by:

Recession and the resulting political pressure

Early signs of a Treasury market collapse (as happened with UK gilts in September)

Contagion from a foreign bond market collapse

In the absence of these factors, I’d be surprised if we didn’t see at least the beginning of a pivot, in the form of a pause in rate rises, by the second quarter of 2023.

Prepping for the pivot

I aim to own a portfolio that can do well in both pre- and post-pivot scenarios.

On the monetary side, if a pivot is executed while the CPI is still elevated, fiat currency will be undermined – the implication being the dollar will be further devalued. Traditional hard money, gold, and superior modern contender, bitcoin, should be winners.

I believe we’re still near the beginning of a commodity up-cycle, driven by supply shortages of essential materials and the expansion of the money supply, resulting in an inflationary decade.

As it gradually dawns on investors that perhaps inflation is not going away, they will seek exposures that benefit from inflation. Commodity companies’ earnings are leveraged to commodity prices, so they could generate multiples of their free cash flows in an environment where other companies’ margins are squeezed.

Note that the real returns of high-multiple ‘growth’ stocks can get destroyed by inflation, as discussed in the Q2 newsletter. ‘Value’ stocks – more specifically those with higher earnings yields, returns on capital and shareholder returns – should outperform.

Natural resources companies come top of the list, in particular:

Energy producers – oil, gas and even coal (possibly uranium)

Producers of the raw materials needed for the scale-up of electrification and battery storage (e.g. copper, nickel, lithium, cobalt)

Copper, nickel, lithium and cobalt are extremely undersupplied to achieve climate targets by the end of the decade. Copper mining is a sector I’m planning to add to the portfolio.

However, I believe the oil rip is likely to come first – possibly even in a recession – such are the demand tailwinds and limited spare capacity, which I will cover in detail in another newsletter.

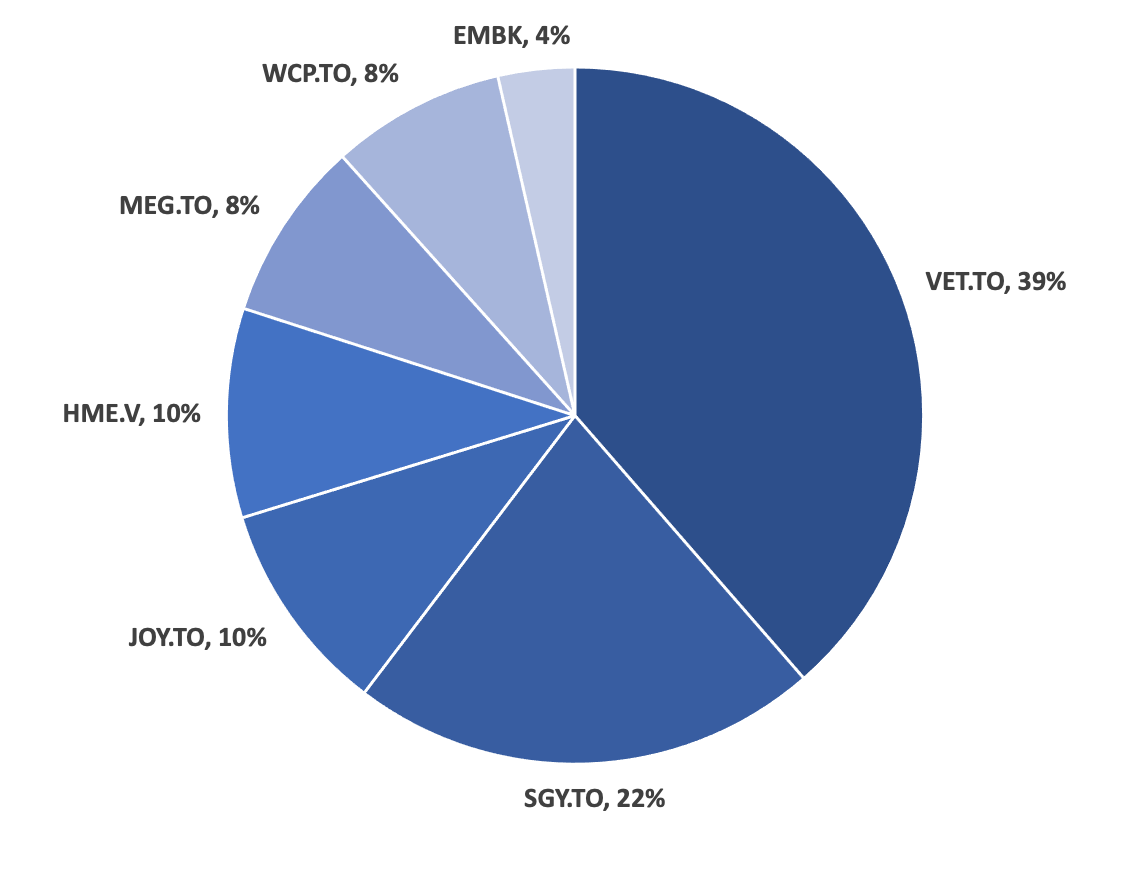

Portfolio

Trades in October

It ended up being a trading-heavy month.

Sold VET calls, TPL

Trimmed VET.TO

Bought HME.V, WCP.TO, MEG.TO, EMBK

Added to bitcoin (outside the portfolio)

Sold VET calls

I sent an email out to the blog mailing list when I sold the Vermilion calls (VET $22.50 Jan ’23 calls). The risk-reward on my calls was no longer looking attractive to me considering recent developments: the current share price, the time getting on, the TTF price crashing and the EU windfall tax. I had to be above $26.30 by 20 January 2023 just to break even, which was not looking like a certainty when the US ticker was only at $22.30 and I was out of the money (a zero at this price come January). Therefore, I cashed out the options for a minor (~7%) loss.

Trimmed VET.TO shares

I also trimmed my VET.TO shares, mainly to get some more exposure to oil-weighted producers (as opposed to the European gas weighting of Vermilion). I went very big with the Vermilion position, although it made sense in the low C$20s, pre-windfall tax, and I may do it again. As you can see, I still have a huge ~40% position and remain bullish on the company.

Sold TPL

I sold my Texas Pacific Land (TPL) shares near the end of October. This has been a big winner – I bought the stock at $630 in 2020, sold some around $1550 and the rest at $2140. In short, it has performed very well, really too well considering its high earnings multiple and disappointing production growth – my thesis was on good production growth. I was wrong, I believe, on likely production growth from here, and the outlook for growth in the Permian now looks far more challenging that I’d anticipated. In addition, the governance at the company is problematic – a proposal to change the ‘cannibal’ (buyback-heavy) nature of the company by issuing shares and making acquisitions (perhaps suggesting management thinks it’s expensive) was a red flag.

Final thoughts

I intended to write an oil macro outlook this month, but such is the length by now, I will have to save it for another time! Perhaps it will be an extra newsletter. I’m planning to dive into researching the copper market and copper producers, in November, and I’d also like to cover Embark Technology (EMBK) soon, an autonomous trucking software company that I bought – for something completely different!

I’d like to thank you all once again for your support as the newsletter has transitioned to paid, and I’m happy to report an encouraging start to paid subscriptions, including one Founding Member. Founding Members get me to work as an analyst for them and receive one company write-up from me on a company of their choice. With any luck, I will be able to publish some of these in addition to the monthly newsletter and company write-up.

With best wishes for the next month,

Timothy Lamb.

Written by Timothy Lamb

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclosure:

The writer owns shares in VET.TO. SGY.TO, JOY.TO, HME.V, MEG.TO, WCP.TO and EMBK at the time of writing.

Disclaimer:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product. Please see the full disclaimer on the About page.