October 2022: Part 2 – The European Energy Crisis

“There are decades where nothing happens; and there are weeks where decades happen.” (Lenin)

This is the feeling for those of us following the European Energy Crisis in the last week of September, and indeed for much of the quarter.

Last week, just as we thought the gas supply constraints from Russia couldn’t get much worse, both Nord Stream pipelines were blown up.

This was something we had considered as a possibility, but the event was nonetheless shocking – potentially a pivotal moment in history that should be the front-page story everywhere.

Russia of course has been blamed – and it could be responsible – although the motivation for Russia destroying its leverage over Europe, when it wants Europe to drop sanctions, is far from obvious.

In terms of what it means for Europe, energy newsletter Doomberg, writes that, according to one veteran of deep-sea oil and gas projects:

“…even with huge government support and perfect international collaboration, it would take at least 20-25 weeks just to get all the specialized equipment and repair materials in place.”

It’s now certain then that there will be no gas flows through Nord Stream this winter and probably even next winter. They may be gone forever.

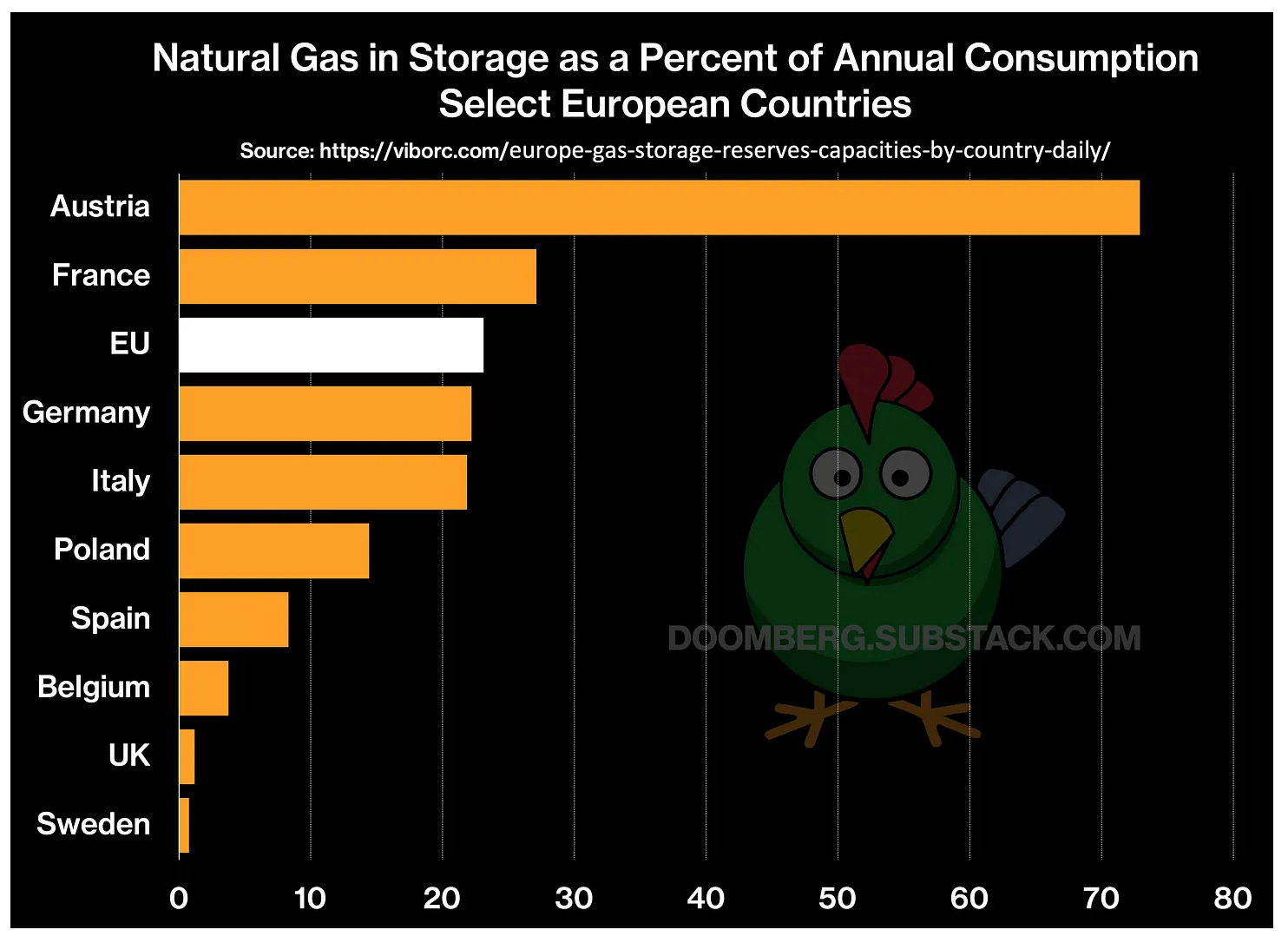

The prospect of zero Nord Stream flows leaves Europe in desperate supply deficit. The fact that storage is near capacity is inadequate to make up for Russian flows as EU storage is less than 25% of average annual consumption.

Even if Europe manages to scrape through a mild winter, there is little prospect of refilling storage from zero next year without the Russian flows that only just made it possible to refill this year. We’re in for a tough winter in 2023/4 as well.

If there is a deep supply shortage, with industry shutting down and widespread blackouts, we could see a social and economic catastrophe. We pray for a mild winter and for early gas to oil switching for power generation.

The EU windfall tax

On Friday 30 September, the EU 27 agreed a windfall tax on energy companies’ ‘excess profits’, as expected. In terms of oil and gas producers, the ‘solidarity contribution’ is set at 33% additional tax on profits over a baseline of 120% of trailing four-year average taxable profit. It will, however, be left up to member states to apply.

We view windfall taxes as the wrong policy for Europe. They should be encouraging as much production and investment in European energy as possible – and this does the opposite. Also, the amount raised from oil and gas producers will not touch the sides of the amount of subsidies given out – as there is simply insufficient domestic production to tax.

Germany’s plan to cap consumer gas prices and pay the difference between the cap and the wholesale price (like the UK plan), encourages consumers to use energy as normal while handing a blank cheque to the energy companies.

Despite the EU’s mandatory target for states to cut electricity use by 5% during peak hours between December and March, and a voluntary target to cut overall electricity use by 10%, unlimited subsidies discourage demand destruction, which is necessary to balance the market. With two countries each offering blank cheques, competing with each other, what’s the limit to the gas price?

A natural gas wholesale price cap was also discussed at Friday’s EU meeting, with 15 countries asking the EU to propose one. This one would be the killer for company profits. However, we see this as unlikely to pass as there is no plan for how it would work without resulting in un-competitiveness and Europe receiving less gas and then fighting over how to divide it up. If it were to pass, it would be a total disaster and would be likely to be reversed.

How this affects Vermilion

We remain bullish on the outsized Vermilion Energy (VET.TO) position and view the EU’s windfall tax as part of the misguided European energy policy that is compounding the continent’s energy crisis.

Investment bank TD Securities published a note on Friday estimating the impact of the windfall tax on Vermilion’s free cash flow (FCF). They estimate the FCF yield for 2023 falling from 57% to 38% at $30 NBP and $35 TTF /mmbtu gas prices.

This is a big hit. However, it still offers a huge FCF yield at relatively modest gas prices, and this projection does not assume the utilisation of tax pools, which could be possible.

Also, it should be remembered the subsidy policies offset the tax to some extent. Without government borrowing and subsidies, many people and companies would be forced to use far less energy in the case of unaffordable prices, which would balance the market at whatever high price. With some governments picking up an unlimited bill, prices will go a lot higher than they otherwise would have. In fact, the net effect of all the energy policies could feasibly result in higher earnings for the energy companies.

With Nord Stream down, a Europe-Russia deal to resume normal gas flows is off the table, and this removes a major risk for Vermilion profits, as high prices for several years now seem almost a certainty.

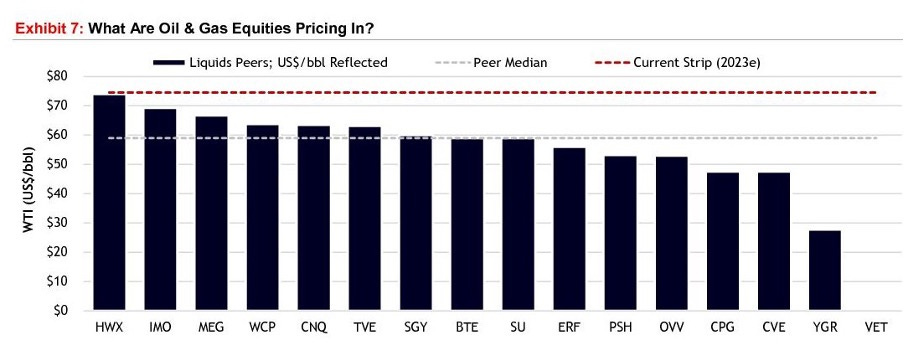

VET remains cheap, and high European gas prices mean investors need have little concern about the effect of oil prices on VET’s earnings: $70 WTI is just fine. However, 50% of production is oil, so it has significant upside there too. Incidentally, this chart we saw on Twitter amusingly has VET priced for $O/bbl WTI! We agree.

My previous articles on Vermilion:

(Note: the Seeking Alpha article was published right at the peak of the August European gas spike, using strip pricing for valuation of the company.)

Gas to oil switching

We also remain bullish on oil, for which – in the already very tight physical market – there are many short- to medium-term tailwinds, even in a global recession.

If we’re wrong about the medium-term – in the case of another black swan event like Covid or a severe global depression – the central problem of underinvestment is not going away, and so we’re confident (bar Armageddon) that we would be in the same undersupplied situation as we are now (or even more undersupplied) on the other side.

We believe the fall in oil since June has largely been due to recession fears – that have been more than priced in – and also technical trading, with insufficient recognition of the tight physical market and supply that has depended on the record US Strategic Petroleum Reserve (SPR) releases that must come to an end.

Oil has some strong tailwinds, including: OPEC+ production cuts, the ending of the US SPR releases (and possible refilling), China reopening, air travel recovering to pre-Covid levels, falling Russian production, OPEC production being near maximum capacity, and gas to oil switching. Virtually any one of these factors alone could result in the oil price soaring.

Gas to oil switching, in light of the European Energy Crisis and high global gas prices, is an underreported risk to the upside for oil. Josh Young, CEO of hedge fund Bison Interests, recently published a well-argued paper on the subject.

He concludes:

“We have conducted our own analysis of oil burning capacity among power facilities in Europe and Asia, and as a lower bound we estimate that there is approximately 810,000 boe/d of installed oil burning capacity in Europe and Asia alone that will come online before this winter—more than 2 times the IEA estimate.

As gas prices remain elevated and electricity remains in short supply in Europe and Asia, we expect installed oil and oil product burning capacity will be utilized near 100% this winter. There is an additional∼8MM boe/d of upside to potential oil demand as non-operating plants are reactivated and operating plants are converted to burn oil. Even if only 10% of this capacity were to come online, it would imply a material 800,000 boe/d of surprise oil demand in addition to our 810,000 boe/d lower bound estimate.”

Personal portfolio

I’ve gone for a very concentrated portfolio of energy companies.

Note, I also own bitcoin, which has not been included in the investment portfolio so far.

For those looking for a hedge or other ideas, I’m interested in the following:

Long a leveraged gold ETF

Short long-dated gilts, with leverage.

Reading recommendations this month

How The World Really Works, Vaclav Smil

Principles For Navigating Big Debt Crises, Ray Dalio

Final thoughts

At this critical juncture for the world, I’d like to express some gratitude for being given a wonderful family and home. I pray for the people of Ukraine, and also of Europe – that the energy security we have all taken for granted to raise our children is restored.

With best wishes for the next quarter,

Timothy Lamb.

Written by Timothy Lamb

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclaimers:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product.

All the content is subject to copyright with all rights reserved. No permission is granted to copy, distribute or modify any text or logos. The content shall not be published, rewritten for broadcast or publication or redistributed without prior written permission from Timothy Lamb.

Those who access this information agree to the following:

While the material is often about investments, none of it is offered as investment advice. This means that neither the receipt nor the distribution of information through this website constitutes the formation of an investment advisory relationship, or any similar client relationship. The materials are not to be relied on for any purpose and are not investment, financial, legal, tax or other advice, recommendation or research.

The materials are for informational and educational purposes only. Educational articles are purely theoretical, with the purpose to enhance financial understanding and education, and members of the public are not advised to in practice follow any of the information provided.

No warranty is given with respect to the correctness of the information provided. Any projections or analysis should not be viewed as factual and should not be relied upon as an accurate prediction of future results.

All information and content on this newsletter is furnished without warranty of any kind, express or implied. This newsletter may contain performance and other data. Past performance is not indicative of future results.

Timothy Lamb will not assume any liability for any loss or damage of any kind arising, whether direct or indirect, caused by the use of any part of the information provided. Timothy Lamb does not warrant that the content is accurate, reliable or correct, or that any defects or errors will be corrected.