October 2023: Treasury Meltdown?

QE a case of "when" and not "if"

“The doom loop occurs as higher interest costs drive higher deficits, forcing the Government to sell more bonds to finance the same… Repeat until there is no market for the bonds.” – EMA GARP Fund, LP., Q3 Report

Nearly everyone has been caught off guard by what’s happening in the US treasury market. Since the start of September, the 10-year yield is up some ~80 basis points, from ~4.15% to ~4.95%, and this is happening as the US is widely expected be near peak interest rates.

Was this anticipated? Certainly not from the outlooks I read from mainstream asset managers. The narrative was that inflation was coming down, the Fed was near the top of its cycle of rate hikes and that it should start to cut in 2024, meaning long-term bond yields should start to fall. In August, this changed to “stickier inflation has resulted in higher-for-longer rates being priced in”. But the 10-year yield has blown out to almost 5.00% when the federal funds rate is only at 5.50%. This does not indicate expectations of inflation returning to target, or large rate cuts, any time soon.

What is really happening here? If asset managers love the higher yields, why are they not snapping up the treasuries and forcing the yields down? There are many factors at play, but one factor that often gets overlooked is the simple supply-demand dynamic.

The rout in long-dated bonds continues

Treasury market: supply and demand

The US debt burden is extremely high, north of 120% of GDP, and the deficit is projected at around 8% of GDP for fiscal year ended 2023, or $2.3 trillion. This deficit percentage, at a time of record low unemployment and a relatively strong economy, is unprecedented. Government spending is up 14% and tax receipts are down 7% year-on-year (as of July 2023). If the economy moves into recession in 2024, the US deficit could be far higher – as high as 20% of GDP, or $5 trillion, according to fund manager Lawrence Lepard of Equity Management Associates.

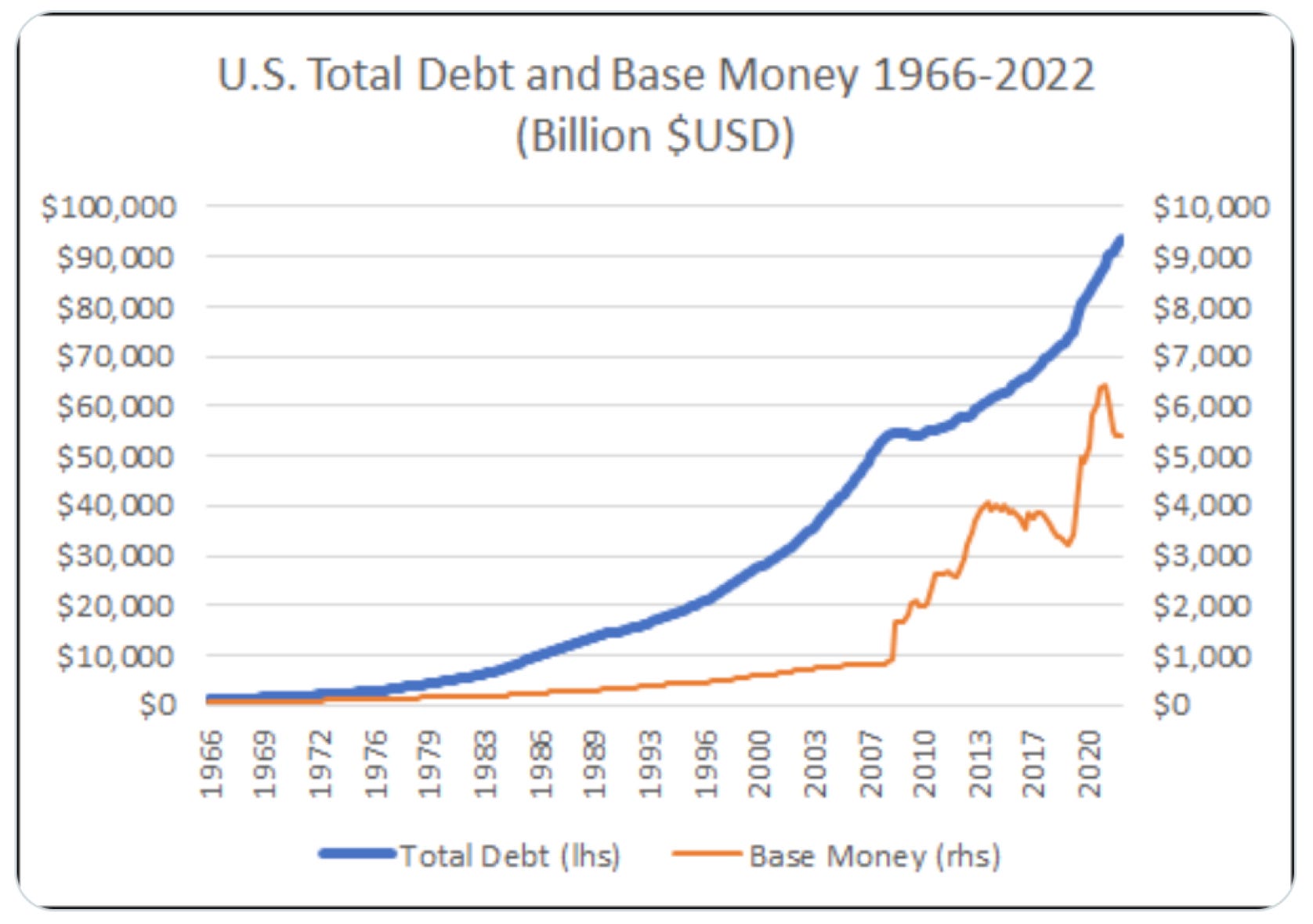

The $33.5 trillion of federal debt is already costing more to service. With the Fed’s rapid rise in interest rates and end of QE, interest payments on the debt have soared to almost $1 trillion and now exceed annual defence spending.

This additional borrowing means all these new bonds are hitting the market at the same as the Fed is engaged in quantitative tightening (QT), letting the treasuries that mature fall off its balance sheet – which then need to be reissued by the US Treasury and bought by the public. In September, the Fed ramped up its QT programme from $47.5bn per month to $95bn per month.

On 4 October, the US national debt jumped by $275bn in a single day, and it was up by $448bn over 2 weeks, the same 2 weeks in which the 10-year yield rocketed by 50 basis points.

The questions we must ask are: who are the potential buyers, at what yields, and will it be enough to balance the market?

While households in the US and institutional investors have been buying, foreign governments are not obliging. The two biggest foreign holders of US debt, Japan and China, have actually been reducing their holdings. With a strong US dollar and high oil prices, foreign governments are incentivised to sell US treasuries to both support their currencies and to buy commodities their economies need, particularly oil. Luke Gromen, founder of macro research firm FFTT, LLC, argues that, unless the dollar and oil both come down, we are at serious risk of a meltdown in the Treasury market (Forward Guidance Podcast: Panic In The Bond Market Will Continue Unless Oil Or Dollar Relent).

Will the Fed be able to prevent such an outcome by ‘jawboning’ on peak rates and rate cuts next year? Maybe for the time being, but what about if the economy moves into recession where the US deficit would be far higher? At what yields will the market absorb the new debt?

Dollar debasement guaranteed

With the debt and deficit where they are, exponential levels of new buyers for Treasuries must be found.

The interest must be paid by more borrowing. Yields have to rise as the supply of new buyers is exhausted, and this compounds the problem further. Higher interest payments mean yet more borrowing which results in higher interest payments. This is the definition of a debt spiral.

At some point then, the Fed has to be the buyer of last resort to keep yields down and allow a functioning bond market to continue to fund the government. The monetary base has to expand exponentially or there will be insufficient capital to buy this exponentially growing debt. We’re heading back to QE in a big way, and this will devalue the dollar against scarce assets over the long run. It's guaranteed. The only question is the timing.

If we go into recession next year, with the increase in the deficit this means, it’s hard to see how we don’t go straight back to QE, and in a bigger way than ever before.

Hard asset businesses in inflation

The central theme of my portfolio has been to position for this long-term inflationary outcome. I’ve switched assets over time as I’ve tried to weigh up the best options. I’ve gone for some hard asset businesses, I’ve gone for high free cash flow and I’ve gone for bitcoin (nice to see the price rip up incidentally over the last week due to the ETF optimism!).

Recently, I read a note by Kuppy (Harris Kupperman, CIO of Praetorian Capital), a top performing hedge fund manager, called Playing Inflation Part 2. The article argues for the merits of buying hard asset businesses at a steep discount to NAV for inflationary periods.

“…what if you want to dramatically outperform during a period of inflation?”, he asks, “In my mind, I want to own hard assets that are trading at a dramatic discount to their replacement costs.”

The idea is that the assets go up in value over a long inflationary period by e.g. 10% a year, but you only pay 30% of the asset value to begin with, so, in theory, your return from inflation alone is 10/30, or 33% a year.

He wants:

high quality and scarce assets

cash flows that will eventually justify the replacement cost of the assets

minimal recurring costs of maintenance

a slightly levered balance sheet

“If you follow this thought exercise through to its logical conclusion, I believe you’ll end up owning lots of companies like St. Joe (JOE – USA) and Valaris (VAL – USA). I should know, as I did this exercise and ended up with those two being the largest equity positions in my fund.” – Harris Kupperman, Playing Inflation Part 2

Performance

YTD: -8% (as at 30 September 2023)

2022: +1%

2021: +10%

2020: +49%

2019: +51%

Portfolio

Trades in September

Trimmed VET.TO, SGY.TO

Sold PSN.L

Bought VAL, JOE, LCA.L

Added to MSTR

Final thoughts

I have been appalled by events in Israel this month. The atrocities committed by Hamas against civilian families including children are really the worst I’ve heard of since WWII. For those of us who believe Israel has a right to defend itself and remove Hamas, while not wanting any civilian casualties, it is a stark reality, and morally troubling, that those two things are mutually exclusive. I have been praying for the people of both Israel and Gaza.

Best wishes as always for the next month!

Timothy Lamb.

Written by Timothy Lamb

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclosure:

The writer owns shares in the securities listed in the stock portfolio at the time of writing.

Disclaimer:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product. Please see the full disclaimer on the About page.