September 2023: Why The Gold Standard Failed

National debts are sky high and are projected to go up indefinitely, government deficits are permanent – and we must borrow more just to make the interest payments.

This sad state of affairs dictates that there will be continued and exponential levels of money creation, a silent tax which debases our savings and takes a cut out of the real returns of equities and especially bonds.

After recently reading Lyn Alden’s new book, Broken Money, I’d like to discuss how the gold standard failed in the twentieth century and why it’s unlikely to work any better in the future. Meanwhile, the best form of money is, for many, hiding in plain sight.

The 1971 US default

At the 1944 Bretton Woods conference, a new monetary order was proposed: all participating governments should peg their currencies to the US dollar – the dollar took over from sterling as the global reserve currency. Meanwhile, the dollar would continue to be pegged to gold at a fixed exchange rate and would be redeemable for gold by foreign central banks. Nations therefore held US Treasury bonds as they were backed by gold and earned a yield.

The fatal flaw was that, while the amount of gold backing the currency was relatively finite, the number of dollars that could be created in the system of fractional reserve banking was unlimited. The system relied on trust – that central banks could exchange their dollars for gold – and political pressure for them not to do so. As long as trust was intact and political pressure was effective, they would continue to hold Treasuries. As soon as foreign central banks started regularly redeeming some of their dollars for gold, however, the system was doomed to fail. And this is exactly what happened.

Between 1950 and 1970, while the number of base dollars in the US doubled, the US’s gold reserves were drained from 20,000 metric tons to 9,000 metric tons due to redemptions from central banks: “dollars became exponentially less ‘backed’ by reasonable amounts of gold” (– Lyn Alden).

The Federal Reserve continued to increase the monetary base, which was multiplied by bank lending. As soon as foreign central banks started redeeming their increased dollar reserves, the game was over – as the US’s gold reserves drew down, creditors then realised the dollar couldn’t maintain its peg to gold if withdrawals continued, so they exchanged even more dollars, accelerating the inevitable fate of the system.

In 1971, President Nixon ended the redeemability of dollars for gold, an effective default, and we entered the modern era of ‘fiat’ currency – where the reserve currency is not backed by anything (save agreements to use the currency for trade and for foreign governments to hold US Treasuries – the Petrodollar/Eurodollar system).

Since 1971, the US dollar has lost 87% of its purchasing power according to official CPI statistics. However, the M1 money supply has increased by around 85 times since that date, suggesting it’s actually a lot worse even than this!

Gold as 21st century money

One might think it was the paper money system that failed rather than gold, and that it might be possible to design a system backed by gold that could work.

The key failure point of gold is that it’s unsuited to use for payment in the modern era. It is heavy, slow and expensive to move around. It can’t be sent on a communications network like the internet (or the telephone line in the last century). It’s also not easily divisible.

This means it’s essential to create ‘paper gold’, IOUs that can be transacted electronically. So now we are trading IOUs, and, unlike physical gold, the supply of promises is unlimited. There is nothing to stop central banks issuing more paper gold – and then the fractional reserve banking system creating leverage on top of this by using the paper to make loans of several times its value. This inflates the money supply, causing debasement of the paper and physical gold alike.

Another problem is that physical gold backing is hard to verify. Bar an independent (and trustworthy) inspection of gold reserves – where they melt down all the gold bars and reform them to check what is in the middle – there’s no way to know for sure the claimed physical gold to paper ratio is accurate.

With any large amount of physical gold, most people will trust a custodian to store it – you must take the risk of it being mismanaged by the custodian or confiscated by a government, for which service you will pay a hefty fee.

Characteristics of the ideal money

The best form of money to hold would be an asset of fixed supply that cannot be changed, that you could easily verify, store and divide, and that you could send quickly and securely over the internet without going through any custodians or other third parties.

There have been some suggestions that a cryptocurrency backed by gold could be the ultimate answer. This is paper gold once again! A blockchain can’t prove that a custodian keeps 1:1 physical gold reserves!

Thankfully, however, such an asset as described above is staring us in the face – it is bitcoin.

Money is a ledger

Bitcoin, like other money, is used as a ledger. With gold, the physical possession of a quantity of the metal proves who owns what. Its rate of supply increase, of around 1-2% a year, is relatively reliable, and it trades at a huge premium to its industrial value solely for this reason – it is the ledger that accounts for most of its value, not the metal itself.

Fiat currencies are ledger systems also: the ledgers are controlled by banks and central banks, which have the power to create money and change the ledger.

Bitcoin is a digital ledger that is immutable.

Bitcoin is better

Fixed supply of 21 million units that will ever exist. Versus gold’s inflation rate that is constant, bitcoin’s trends to zero. Technological developments or high enough prices will incentivise miners to increase the supply of gold past its 1-2% inflation rate – there is an enormous amount of untapped gold on Planet Earth – not so with bitcoin.

Easily verifiable – to prove what you own, send and receive – as all the transactions are published independently by the entire global network of computers (or ‘nodes’).

Permissionless, peer-to-peer digital payment network – you can quickly send the asset from London directly to someone in Argentina without any banks or intermediaries being able to stop you (on the Layer 2 Bitcoin Lighting Network the recipient will have the money instantly and it costs virtually nothing). Imagine trying to do that with gold!

Transportable – all you need to take with you are your 12 or 24 key words to access your bitcoin. You can even store them in your head. You can take it with you on an aeroplane or when fleeing a warzone.

Automatically divisible into 100 million parts.

Smartphone enabled payments – you just scan the merchant’s QR code with a Lightning enabled app. Instant settlement.

No need to use paper bitcoin – as the asset has all the properties we want in a monetary technology, there’s no need to use paper bitcoin. It’s easier to use the real thing. And, as it’s so easy, people will (or certainly should!) be disposed to use and demand the real thing rather than IOUs.

The Bitcoin network is decentralised and secure. It is maintained by hundreds of thousands of computers around the world, and neither the network nor the protocol is governed by any organisation. Governments cannot control it and they can’t create more bitcoin. The Bitcoin blockchain database has never been hacked. Hacking one computer’s database will not corrupt the others.

So long as all the decentralised and independent operators of Bitcoin network do not unanimously act against their own self-interest and decide to debase themselves by issuing more coins (which seems virtually impossible), we know exactly what the monetary policy is.

A bitcoin standard?

Bitcoin is likely to run alongside government issued currencies for a long time. When the current order of fiat currency ultimately fails, the US may not go straight to bitcoin as it’s such a departure from recent monetary policy – they can’t print it and they can’t control it.

The US may try gold again, or a basket of commodities, to back a paper currency. This will not be a problem for bitcoin as, once again, the IOUs will inflate while bitcoin’s supply growth trends to zero.

They may try to issue central bank digital currencies (CBDC), a worse form of fiat, as China has with the digital yuan. We pray not, as the level of control a government would have over its citizens could be used for totalitarian ends. Governments could dictate how we spend our money – these would effectively be government credits.

Historically, people have ultimately flocked to the hardest money available to them. The gold standard moving to fiat currency was the exception – because gold didn’t have the utility needed in the modern world – the utility that bitcoin has in spades.

Performance

YTD: -13%

2022: +1%

2021: +10%

2020: +49%

2019: +51%

Note: my BTC position was added into the portfolio – from existing holdings outside of the portfolio – at the end of March. The positive performance year-to-date of that position has therefore not been recorded in the performance numbers.

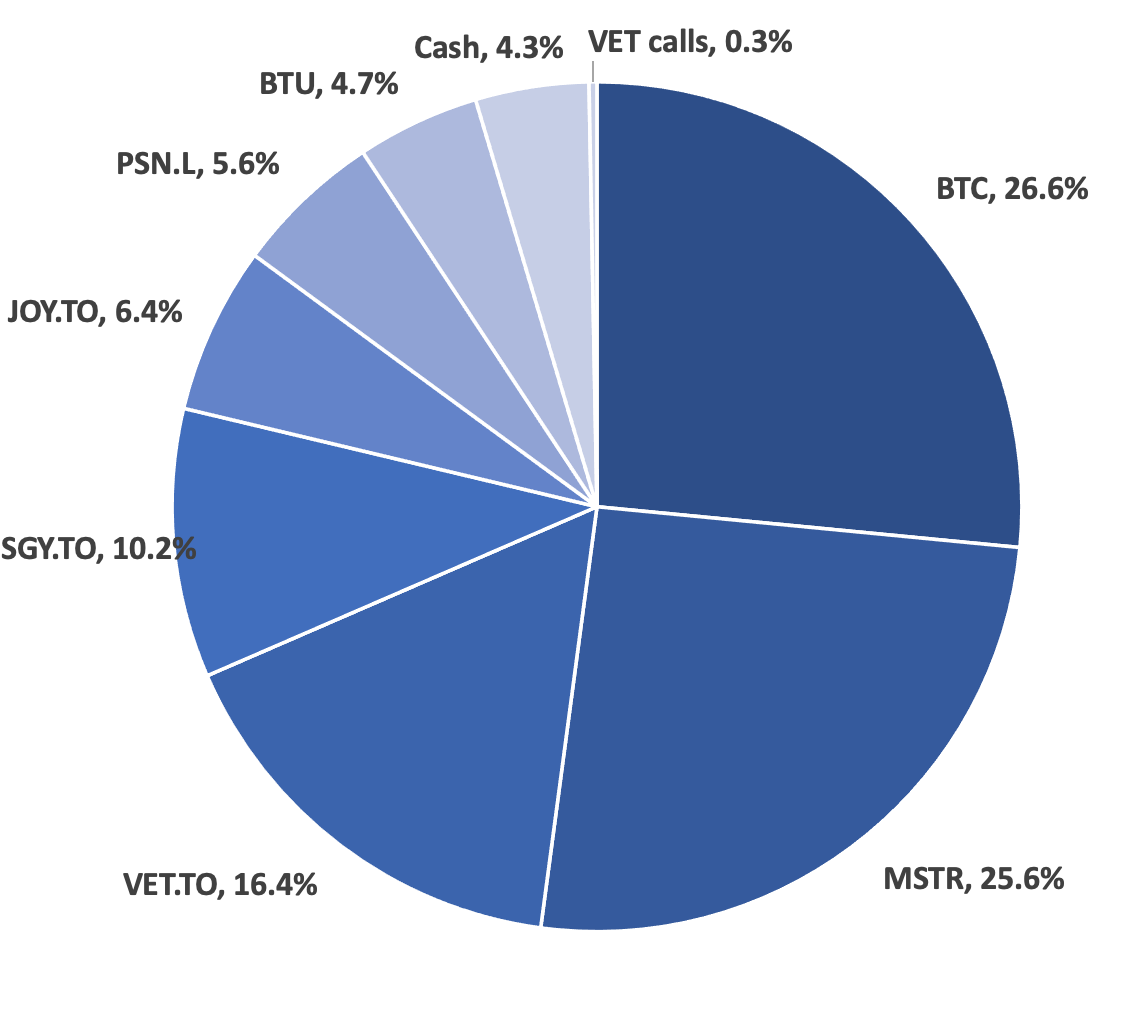

Portfolio

Trades

I sold my gold, silver, copper and iron ore stocks (SSL.TO, WPM.TO, TECK and MSB) to buy more bitcoin and MSTR, and I also withdrew some cash from the portfolio.

Final thoughts

It’s been a great summer. We’ve spent a lot of time at castles, beaches, gardens, zoos, all the things toddlers love!

Best wishes for the autumn!

Timothy Lamb.

Written by Timothy Lamb

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclosure:

The writer owns shares in the securities listed in the stock portfolio at the time of writing.

Disclaimer:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product. Please see the full disclaimer on the About page.

Any writeups about:

- WPM.TO

- TECK

- MSB

?