Undervalued Report: Hemisphere Energy

A Canadian oil junior with turbocharging growth potential

Dear subscriber,

Here is the first Undervalued Report: a monthly deep dive on an undervalued company.

The moment has arrived: this Substack is becoming a paid subscription newsletter. Subscribers will receive the thematic newsletter and a company deep dive every month. Free subscribers will be able to read the opening sections of the Substack articles – and the blog, retailbull.co.uk, will remain free.

I am going to be covering various sectors in the monthly write-up – wherever opportunities arise that I can get my head around – but energy remains a key area of focus at the moment. For the first Undervalued Report, you’re getting a corker of a company – one I have recently bought – and this one is oil.

Thank you to all of you for your interest and support thus far!

Hemisphere: a Canadian oil junior with turbocharging growth potential

Hemisphere Energy (HME.V) is a junior Canadian oil producer with conventional assets in Alberta and a market cap of C$150m.

The company is optically cheap, being at a >50% discount to net asset value (NAV) and offering a 27% free cash flow yield at $87 oil. It paid a variable dividend of 7% annualised during Q3 and is buying back shares in addition to growing production. It has huge torque to higher oil prices and also offers some protection from a downturn – as it has virtually no debt and exceptionally low-decline assets.

The stock has almost no institutional ownership – there will be very few analysts, if any, covering it. Therefore, it’s not altogether surprising that the market has completely overlooked the major impact on cash flow of the company’s potential continued rapid growth.

HME.V stats

Share price: C$1.43

Share count: 105m

Market cap: C$150m

EV: C$154m

Production: 2,900 boe/d (Q2), 99% heavy oil

Dividend yield: 7% (variable)

Contents

Assets

Production

Free cash flow

Hedges

Capital allocation

Management

Valuation

Risks

Final thoughts

Assets

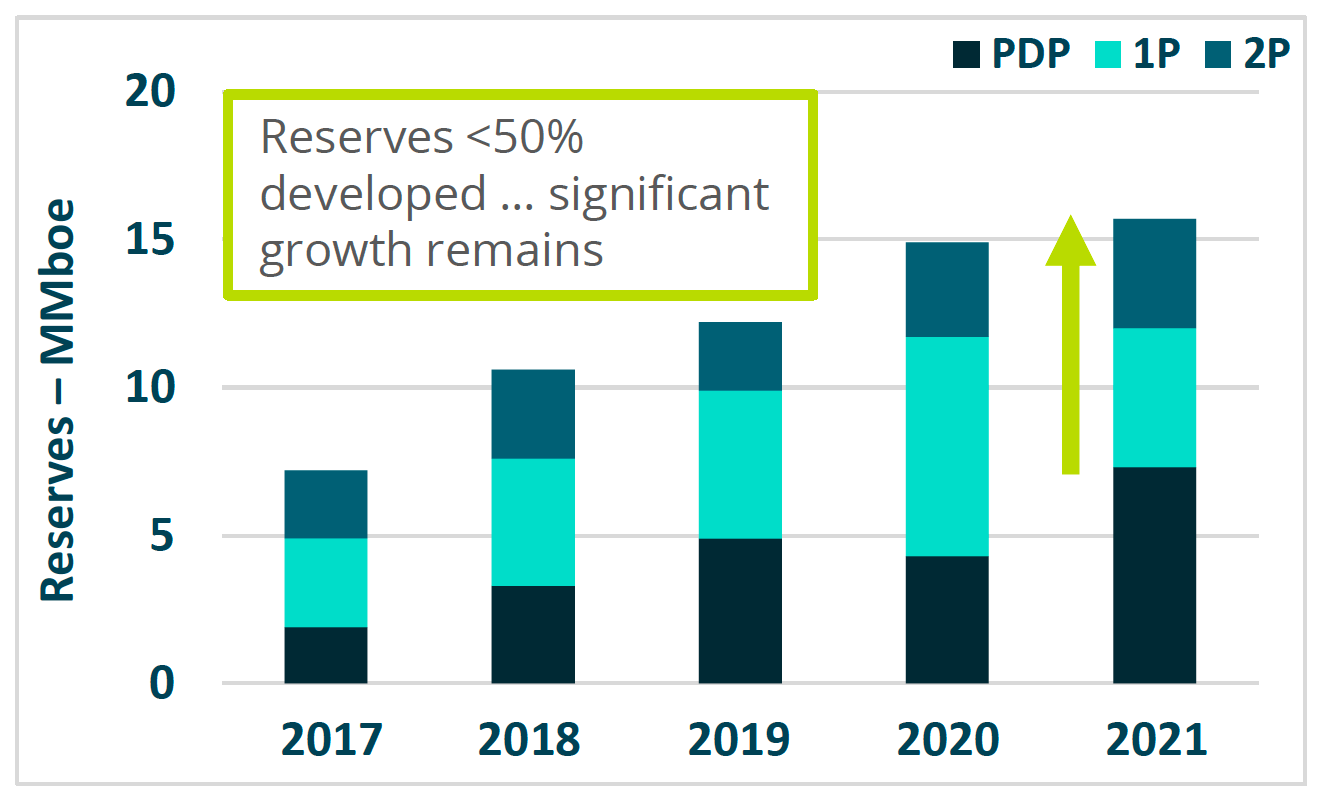

Hemisphere focuses on the growth of its low-decline heavy oil pools, using enhanced oil recovery methods: waterflooding and polymer flooding. It operates two conventional oil pools at Atlee Buffalo in Alberta, the Mannville F pool and the Mannville G pool, and has a proved Reserve Life Index (RLI) of 18 years.

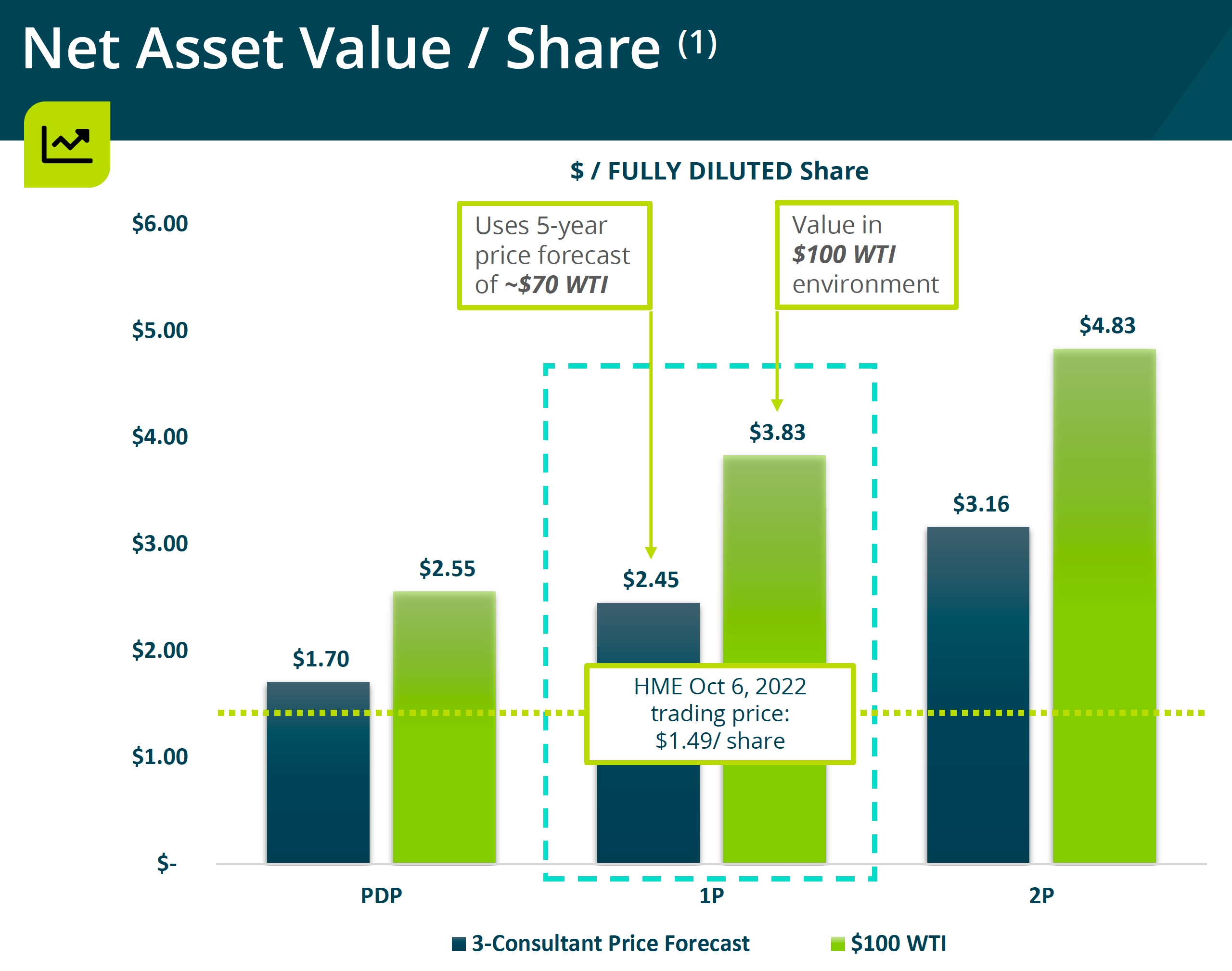

This reserve report, suggesting 2P reserves of over twice the enterprise value (EV) is at $69/bbl WTI.

This results in a NAV per share of C$3.16 at $70 WTI and C$4.83 at $100 WTI.

Hemisphere has minimal liabilities, with only C$3.6m of net debt at the end of Q2 and decommissioning liabilities of C$7m.

Production

In Q2 2022, production averaged 2,900 boe/d, 99% of which was heavy crude oil.

Production has been rocketing. July’s production of 3,150 boe/d is 73% higher than the 2021 average of 1,820 boe/d.

The increase is due to Hemisphere’s enhanced oil recovery projects (polymer flooding) and the drilling of seven new wells. The Upper Mancille G pool was converted from waterflood to polymer flood in 2021 and three new wells were drilled there. The annual report says that they have been producing 80% more from the pool than they were before the polymer injection.

The polymer flood at the F pool has now also been started up, and there were up to four additional wells planned to be drilled in the third quarter.

Reserves remain less than 50% developed and the company says, “significant growth remains”:

Hemisphere has consistently beaten its production targets lately, so we are optimistic 2022 exit production could even be higher than the forecast 3,300 boe/d.

Free cash flow

In the Q2 report, adjusted funds flow (AFF) was C$14m and free cash flow (FCF) was recorded at C$8.25m. This is arrived at simply by deducting total capital expenditures (C$5.8m) from AFF.

However, the company spent a lot of this capex on growing production. What we want to know is what the actual FCF is when just keeping production flat.

They kept production flat (increased by 2%) in 2020 while only spending C$1.7m on capex for the whole year. And this money was not strictly spent on maintaining production. CEO Don Simmons, in the 2020 annual report, writes:

“This capital was dedicated to expanding our waterflood injection pattern and preparing for polymer flood conversion in the Atlee Buffalo G pool.”

“Maintaining production with minimal capital spending and no drilling activity was a key corporate goal. We managed to obtain 2% year over year growth in average annual production at just over 1,700 boe/d (99% heavy oil). Negligible overall production decline, and subsequent incline from waterflood conversions, is a testament to our stable, high quality oil reserves.”

In 2020, the decline, and therefore the capex needed to maintain production, was virtually zero.

However, we’ll be conservative and use the C$1.7m maintenance figure, and we’ll double it as production is higher now – and then divide by 4 for the quarterly figure: C$0.9m (let’s call it C$1m).

C$14m AFF minus C$1m maintenance capex = C$13m FCF for Q2.

In addition, the company lost C$2.5m on hedging in the quarter: the unhedged FCF would be C$15.5m.

On Q2 prices, this results in a hedged FCF yield to EV of 34% annualised, and an unhedged FCF yield of 40% (using average Q2 production).

The unhedged FCF yield to EV is 20% at $80 oil, and, conveniently, you can add ~10 percentage points to that for every $10 increase in the oil price from there, giving the company a lot of upside for a sustained higher oil environment: i.e. 39% at $100 WTI, 58% at $120 WTI.

The company’s breakeven is around $60 oil.

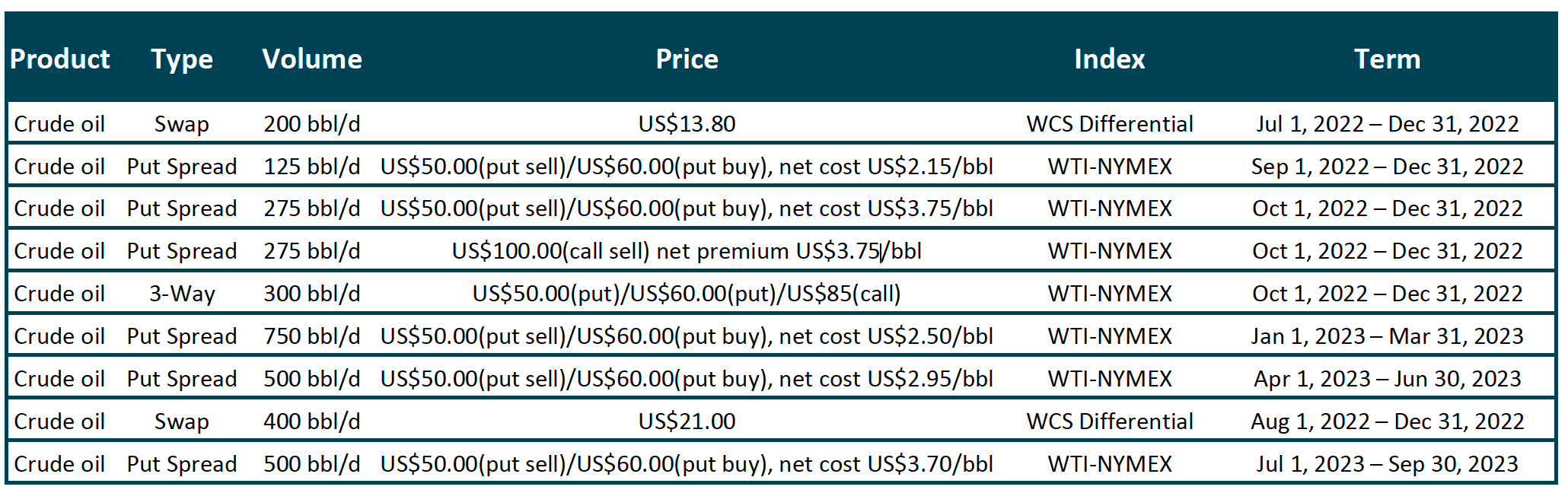

Hedges

The hedging book was recorded as a liability of C$3.1m in the Q2 report. A lot of the hedges rolled off at the end of August.

Capital allocation

In June, Hemisphere announced a variable dividend targeting 30% of FCF to be paid quarterly. The dividend of C$0.025 per share, paid in Q3, gives a competitive 7% annualised dividend yield.

“The remaining 70% of free funds flow may be used for additional spending on Hemisphere’s Normal Course Issuer Bid (NCIB) and/or other special dividends, in addition to possible strategic acquisitions and accelerated investments in the Company’s long-term development program.” (Source: Q2 report)

This capital allocation framework attracts me as I get a good dividend, based on a percentage of FCF rather than a fixed amount – so the dividend will benefit from production growth, oil prices and buybacks: this is important. The prospect of buybacks and special dividends on top is also welcome. Note though, the dividend will be based on their FCF figure (after capex) rather than ours.

The company has repurchased 5.2m shares since September 2019, and the fully diluted share count has come down since December 2019 from 110.8m shares to 105m. I’m optimistic the capital returns will increase once the debt is paid down to zero, which could have happened in Q3.

Management

Insider ownership is high, at 15% of the shares, which bodes well. CEO Don Simmons owns around 3% of the company.

Simmons, a geologist by background, became CEO in 2008. I’ve been back to read all his shareholder letters in the annual reports since 2012 (which is the earliest available on the company’s website) and I’m impressed. His tone reminds me a little of Buffett’s letters, where he views shareholders as partners along for the ride alongside him for the long term. Also, he’s delivered (or overdelivered) on the promises he’s made in the past.

From 2012 to today, while at the helm, he’s increased reserves from 1.3m to 15.7m boe, and has increased production from 408 boe/d to July’s 3,150 boe/d. Over the period, the share count has only doubled and the company has paid back almost all debt taken out – despite most of this time being a low oil price environment where many junior competitors went bust.

Valuation

8 x FCF minus net debt

The valuation model of 8 x FCF minus net debt (often used for valuing E&Ps), at $87 WTI, results in a market cap ofC$324m, or C$3.09 per share – more than twice the current market cap.

NAV per share

Using NAV, the proved + probable (2P) NPV10 is C$351m, or C$3.34 per share, at ~$70 oil.

Neither of these metrics, however, fully account for the impact of the company’s production growth on the ‘owner earnings’: the amount of capital an owner of the whole company could extract from it over its lifetime. Production growth in the near term brings forward the future cash flows that are discounted from further out using the NPV10. Increased exploration can also add to the reserve value.

Discounted cash flow model

My preferred method of valuation is a discounted cash flow (DCF) model.

Here I have projected that HME’s production growth continues its upward trend, reaching 5,000 bbl/d in 2025 and flatlining thereafter.

The results, with production growth to 5,000 bbl/d in 2025, give a value per share of:

Negative real value at C$60 WTI

C$1.46 at $70 WTI

C$4.44 at $87 WTI

C$6.91 at $100 WTI

C$10.51 at $120 WTI

The company is priced for $70 oil and there is 3x potential, in real terms, for a buyer of the business – assuming current oil prices for the next decade.

And, as you can see, with its relatively high breakeven, it has exceptional torque to higher oil prices.

Explanation of the DCF model

My FCF figures for 2022 include the amount spent on capex for production growth.

The amount of FCF that is reinvested to grow production is recorded in the ‘Of which capex’ column. I have started with C$12m in 2022 – which is the company’s C$16m figure for its 2022 capex programme minus our C$4m figure for the capex needed to keep production flat (discussed earlier in the ‘free cash flow’ section).

I have then accounted for increasing maintenance capex as production grows, by adding C$1m per year, up to C$15m in 2025. From 2026, we can remove the growth capex, as production is staying flat, and we are left with the C$4m additional maintenance capex. (I’ve then grown this figure for the remaining years to account for inflation and natural decline.)

The capex figures are then subtracted from FCF to get the ‘owner earnings’ (the amount an owner of the business would be able to take in dividends).

We give the business a terminal multiple of 4x FCF in year 10. We discount this figure and the ‘owner earnings’ back to today at a 10% p.a. discount rate. We add these numbers together and subtract net debt to arrive at the value of the equity today. Divide by 105m to get the per share numbers.

Risks

The biggest risk for a buyer of the company is a sustained WTI oil price below $70, in which case the equity is worth less than the current price, according to my DCF.

A short-term fall in the oil price, however, is not a great risk to a long-term owner. The company has next to no debt, its low decline assets mean that maintenance capital is negligible, and it can cut the growth capex, as it demonstrated in 2020.

Other risks include capital allocation – the company could, for example, engage in a poor acquisition which could destroy value.

Production growth is also an uncertainty – the company’s polymer flooding may not continue to be as successful with new wells as it has been in recent quarters. Our 5,000 bbl/d target by 2025 is based on past results and what appears possible from the assets and management’s trajectory – but it may not happen.

Final thoughts

Hemisphere looks like a strong contender by any valuation methodology. It has exceptional, low-decline assets and is at a >50% discount to NAV. Its FCF yield (20% at $80 WTI oil and ~40% at $100 WTI) puts it well up in the mix of its Canadian competitors. Unhedged, it has some amazing torque to high oil prices: a 99% oil production mix and a sensitivity of ~10 percentage points of FCF yield for every $10 increase in the oil price.

What’s being completely missed by the market is the impact of the company’s potential rapid production growth. If it can grow production to 5,000 bbl by ~2025, this turbocharges the company, making it capable of rewarding long-term owners with real returns of ~C$4.40 per share at $87 WTI, ~C$6.90 at $100 WTI and ~C$10.50 at $120 WTI.

If looking for a company to take advantage of a multi-year energy bull cycle – but one with reduced risks of bankruptcy in the case of a downturn – this should be high up the list!

Thank you for supporting The Undervalued Newsletter!

With best wishes,

Timothy Lamb.

Written by Timothy Lamb

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclosure:

The writer is long HME.V at the time of writing.

Disclaimers:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product.

All the content is subject to copyright with all rights reserved. No permission is granted to copy, distribute or modify any text or logos. The content shall not be published, rewritten for broadcast or publication or redistributed without prior written permission from Timothy Lamb.

Those who access this information agree to the following:

While the material is often about investments, none of it is offered as investment advice. This means that neither the receipt nor the distribution of information through this website constitutes the formation of an investment advisory relationship, or any similar client relationship. The materials are not to be relied on for any purpose and are not investment, financial, legal, tax or other advice, recommendation or research.

The materials are for informational and educational purposes only. Educational articles are purely theoretical, with the purpose to enhance financial understanding and education, and members of the public are not advised to in practice follow any of the information provided.

No warranty is given with respect to the correctness of the information provided. Any projections or analysis should not be viewed as factual and should not be relied upon as an accurate prediction of future results.

All information and content on this newsletter is furnished without warranty of any kind, express or implied. This newsletter may contain performance and other data. Past performance is not indicative of future results.

Timothy Lamb will not assume any liability for any loss or damage of any kind arising, whether direct or indirect, caused by the use of any part of the information provided. Timothy Lamb does not warrant that the content is accurate, reliable or correct, or that any defects or errors will be corrected.