Undervalued Report: Sandstorm Gold

Undervalued Report: Sandstorm Gold

Growth and dormant assets set to turbocharge the stock in a gold bull market

With ballooning national debts over recent years and underinvestment in commodity production, there is a strong case for continued bouts of inflation and currency devaluation over the longer term. Sound money assets, like gold and bitcoin, should shine.

How does one gain exposure to gold? Physical gold and silver, an ETF, an ETF of miners or do you buy individual mining stocks? As a value investor, my preference is to buy a company that produces free cash flows and grows.

The best upside to a precious metals bull market in the short term will come from some small cap and leveraged producer that no one has heard of and that is barely even profitable at current prices. But mining is an extremely tough sector, and one can easily lose a lot of money investing in these kind of stocks.

For the generalist investor like me – and also if concerned about the possibility of a broad inflationary environment, as I am – the royalty model is particularly attractive. In the case that this gold bull market we expect doesn’t materialise for a long time – or even if it doesn’t happen at all or we have a falling commodity price environment – royalty companies can still produce free cash flows, grow and outperform.

The royalty model

Royalty and ‘streaming’ companies are vehicles that collect royalty cheques for a percentages of a mine’s revenue or, in the case of streaming, have the right to purchase a percentage of a mine’s production for a (typically very low) fixed cost or a fixed percentage of the spot price. They have no capex or exploration costs, unlike miners; the only expenses are to pay the small staff and the admin costs to collect the cheques and reinvest the proceeds into more contracts.

In a broad and sustained inflationary environment, where prices increase across the board, rising commodity prices may not translate to higher profitability for miners if their production and labour costs also increase. Royalty companies, so the theory goes, would actually benefit from such a scenario as they get the upside from commodity prices without the downside of higher capex costs.

Sandstorm Gold (SAND / SSL.TO) – stats

Share price: $4.90 (22 Feb intraday)

Share count: 299 million

Market cap: 1.5bn

Net debt: $490m

EV: 2.0bn

Overview

Sandstorm Gold is a gold royalty and streaming company, headquartered in Vancouver. Its business model is to make upfront payments to miners to help finance mining operations – in exchange for royalties and streams on commodity production. For royalty contracts, Sandstorm receives a fixed percentage of revenue from a mine’s production; for streams, the company gains the right to purchase a percentage of a mine’s commodity production at a fixed price or a fixed percentage of the spot price.

The company is focused on gold, with 70% of 2022 production being gold and silver, and over 70% of 2025 production forecast to be purely gold. It also has exposure to copper and diamonds.

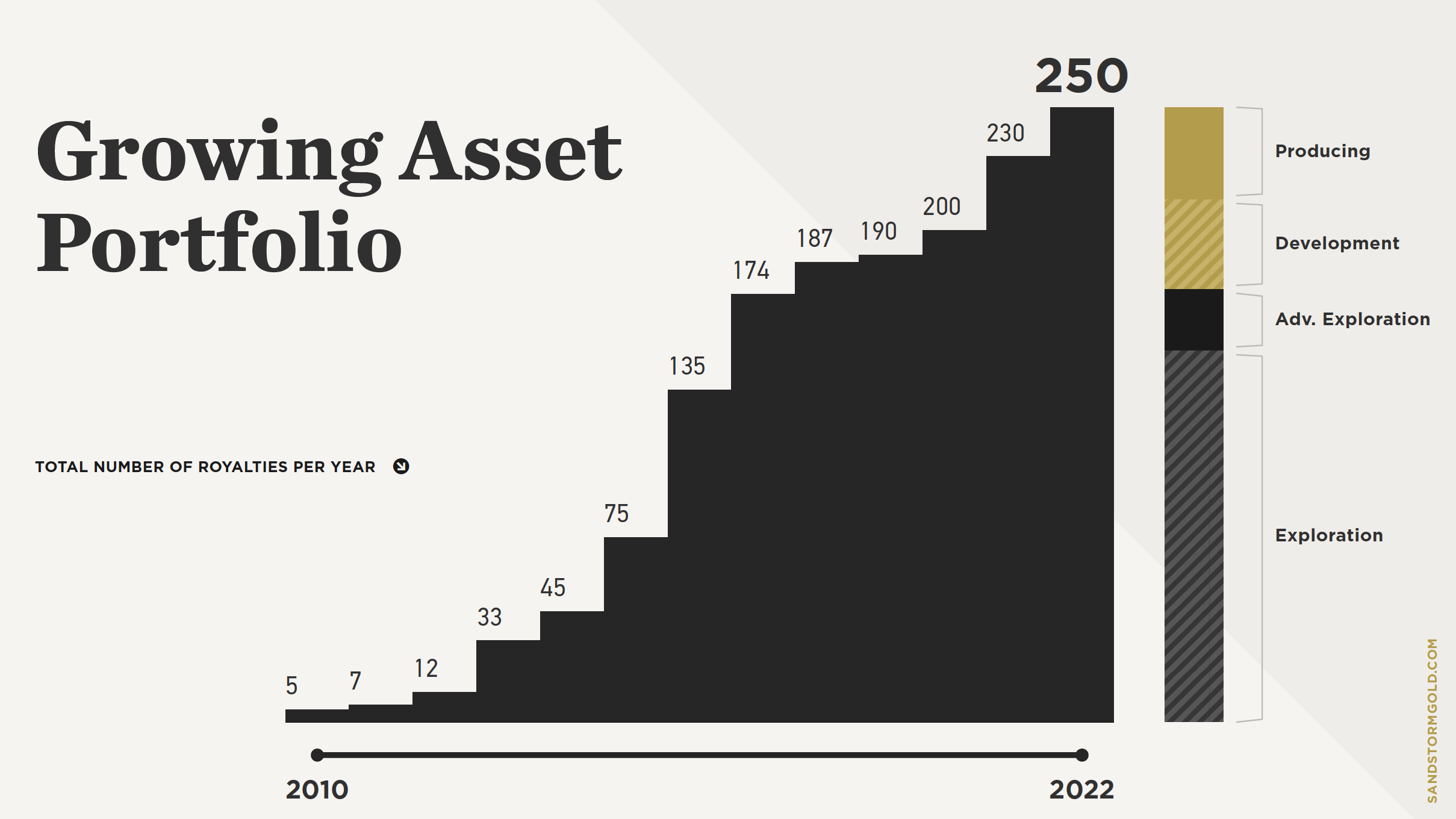

It has 250 royalties and streams, of which only 39 are cash-flowing. With no asset contributing more than 15% of the company’s consensus net asset value (NAV) and the top five assets contributing 42% of NAV, it has the most diversified portfolio in the royalty and streaming segment. It also has the lowest cost mines exposure.

Sandstorm is like an iceberg, where the producing assets are the only part that shows up on earnings but there is a lot more below the surface. These mines in exploration stage can be seen as dormant assets.

Every year at Sandstorm, bar 2020, production has increased, and more gold equivalent ounces (GEOs) are discovered than are produced. It’s the highest growth company in its segment with ~70% production growth forecast between 2022 and 2025. Gold equivalent production was 82,000 ounces in 2022 and is expected to rise to 140,000 in 2025.

Acquisitions

Issuing shares for acquisitions in 2022 has undoubtedly hit the share price, and the stock has underperformed. Nomad Royalty shareholders received Sandstorm shares in the acquisition deal, and, according to management on the annual results call, they mostly sold these shares which has put a lot of pressure on the price.

However, Sandstorm has transformed its royalty and streaming portfolio with these deals and now has industry-leading diversification, the lowest cost mines in its segment and a ~70% growth profile to 2025.

In 2022, Sandstorm completed two transformative acquisitions for $1.1bn:

In July, Sandstrom acquired nine royalties and one stream from BaseCore Metals LP for $425m in cash and 13.5 million shares of Sandstorm. Three are on currently producing assets.

In August, the company acquired Nomad Royalty Company for 74.4 million Sandstorm shares. Nomad, the highest growth precious metals royalty company, had 20 royalty and stream assets, of which seven are producing. Sandstorm expects production from the Nomad deal to grow to 35,000 GEOs by 2025. Nomad was acquired at 0.9x NAV and the transaction increases Sandstorm’s long term production guidance by approximately 50%.

Management

Sandstorm has a strong CEO in Nolan Watson, who co-founded the company in 2008 and has led the company’s transformation. Prior to Sandstorm, Nolan was Chief Financial Officer of Silver Wheaton (now Wheaton Precious Metals) where he developed the silver streaming business model and helped to raise more than $1bn in debt and equity to fund the company’s growth.

Financials

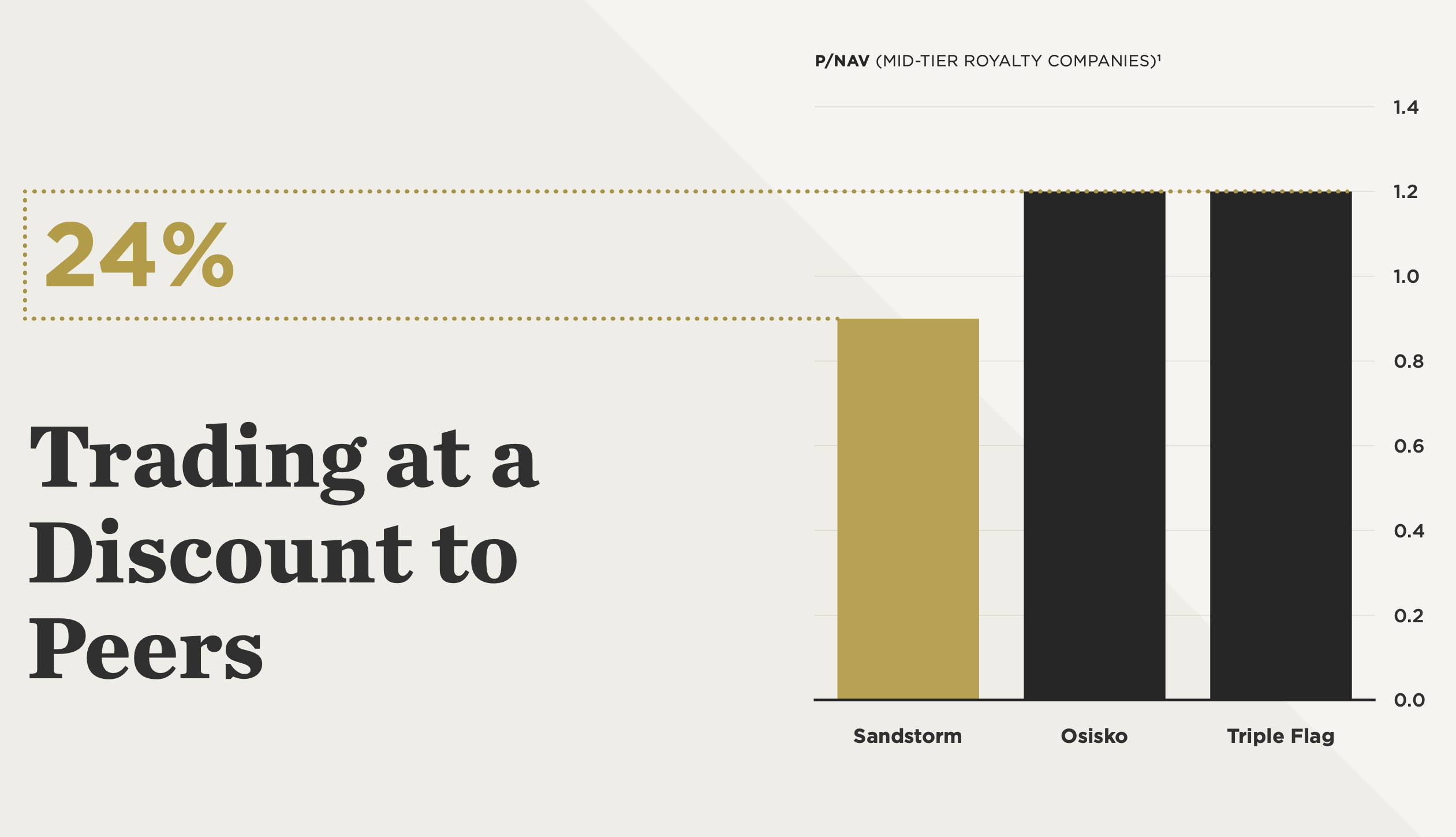

Sandstorm, at a $1.5bn market cap, is trading just marginally over its book value of $1.4bn, and at ~0.9x consensus NAV. This is a substantial discount versus peers, and a royalty company of its quality, growth profile and diversification could easily trade at 1.5x NAV.

Net income was $79m for 2022, but this includes a large depletion expense and also gains on the disposal of investments and streams – we have to remove these to get a more accurate picture of the free cash flow (FCF).

With revenue of $149m, minus:

$23m cost of sales (excluding depletion)

$13m admin expense

$7m project evaluation

$17m finance expense

$5m tax

…I make the FCF out to be around $100m. The enterprise value sits below $2bn, so we are paying around 20x 2022 FCF for the company (less if you subtract Sandstorm’s equity holdings of ~$150m).

This seems a pretty good deal to get a 5% FCF yield at 2022 commodity prices with the growth that Sandstorm has in store. If it can increase production by 70%, as planned, by 2025, at 2022 commodity prices, it will be priced at just 11-12x FCF. It should have paid off a lot of the debt by then as well, further reducing the multiple.

Capital allocation

Sandstorm began paying a quarterly dividend of C$0.02 per share in Q1 2022.

Following the 2022 acquisitions, the company has ~$490m of net debt, which the company announced in the recent conference call that it plans to pay off by the end of 2026. They are in “consolidation phase”. This then will be where the free cash flow goes for the foreseeable future, so do not expect increases to the dividend until the debt is paid down.

Horizon Copper and Sandbox Royalties

Sandstorm owns equity and convertible debt in Horizon Copper and Sandbox Royalties, valued at around $150m.

Formerly Royalty North, Horizon Copper is a copper-focused royalty company. In August 2022, Sandstorm closed a transaction with Horizon Copper in which it exchanged its 30% interest in the major Hod Maden project in Turkey (in addition to other considerations) for a $200m gold stream on Hod Maden production, a 34% equity stake in Horizon and a convertible note. Under the terms of the Hod Maden deal, Sandstorm can buy 20% of all gold produced from Hod Maden at 50% of spot price until 405,000 ounces are delivered, and 12% of gold production at 60% of spot price after that.

Sandbox Royalties (previously Rosedale Resources) is a new royalty company created by Sandstorm Gold and Equinox Gold in May 2022. The idea is that Sandbox will take on from Sandstorm the royalties on other commodities, including copper, zinc, graphite and uranium (in addition to some gold and silver), to keep Sandstorm focused on precious metals, and Sandbox will seek a public listing. In June 2022, Sandbox acquired a portfolio of royalties from Sandstorm and Equinox. In exchange, Sandstorm received 34 million shares of Sandbox, cash and a convertible note. Sandstorm owns 20.1% of the company.

Risks

The major risk of course is commodity prices. Despite its lower risk business model as a royalty company, Sandstorm would not be immune to falling gold prices. Under a flat pricing environment, however, I believe a lot of the pricing risk is removed at 0.9x NAV. Could it trade at 0.7x NAV? Anything can happen in markets, but I don’t see it as likely, and this would be a great buying opportunity.

Why I like Sandstorm

Sandstorm is a high quality and growing company at a reasonable price. It has an incredible record of building from five royalties in 2010 to 250 today; production has risen every year, apart from in 2020, in a lacklustre commodity market. Sandstorm should continue its past business performance and grow its assets, almost regardless of commodity prices.

Yet, it is set to thrive in a precious metals bull market, with or without broader inflation, due to its low fixed costs, high margins and dormant assets. It has a compelling growth pipeline, and the vast majority of its royalty and streaming contracts are in exploration stage. Right now, these non-producing contracts are attributed very low value as there is no appetite for a gold capex cycle. If, however, the gold price were to go significantly higher, some of these assets would likely go into production and turbocharge the stock.

I’ve been making use of the poor sentiment due to the share issuance to accumulate shares as my exposure to gold.

Thank you for supporting The Undervalued Newsletter!

With best wishes,

Timothy Lamb.

Blog: www.retailbull.co.uk

Twitter: @theretailbull

Disclosure:

The writer owns shares in Sandstorm Gold at the time of writing.

Disclaimer:

This article is for informational purposes only, does not offer investment advice and does not recommend the purchase or sale of any security or investment product. Please see the full disclaimer on the About page.